Your guide to IFRS 16 Lease Accounting (IFRS 16 Standard)

Updated on : 14 Jun 2022

Published : 14 Jun 2022

KPI

![]() TABLE OF CONTENTS

TABLE OF CONTENTS

![]() TABLE OF CONTENTS

TABLE OF CONTENTS

The new phrase in the accounting rules is International Financial Reporting Standards 10 or IFRS16. The International Accounting Standards Board (IASB) adopted IFRS 16 in January 2016 and it went into effect on January 1, 2019. The old leasing Standard, IAS 17 Leases were replaced by IFRS 16.

The adoption of the new IFRS 16 lease standards is likely to have a number of positive implications, the most notable of which is an increase in leased assets and financial liabilities on the lessee's balance sheet. Understanding the impact of IFRS 16 on your company early on can help you sort out difficulties and cut down on implementation costs and compliance risk.

There are various aspects of the IFRS 16 that must be understood. Let's get started!

What is IFRS 16?

The IFRS 16 Leases fill in the voids left by IAS 17 Leases. The new standard requires that all businesses, particularly those with recurring leases, report lease liabilities and accompanying Right-Of-Use Assets in their financial statements

Impact of IFRS 16 on Business Accounting

IAS 17 "Leases" and related interpretations on leases, as well as IRRIC 4, SIC 15, and SIC 27, are all replaced by IFRS 16 "Leases." It applies to companies with annual reporting periods that begin on or after January 1, 2019. The IFRS 16 provides guidance and standards for the recognition, measurement, presentation, and disclosure of leases.

Understanding a Lease

A lease is a contract (or a part of a contract) that grants the right to govern the use of a certain asset for a set period of time in exchange for a fee. All contracts must be scrutinized to see if it contains a lease. The IFRS 16 definition of a lease is substantially broader than the IAS 17 term.

The following should

- Identifying the leased asset

- Choosing how to use the leased asset

- Who receives the majority of the economic gains

- Does the supplier have the right to replace the asset?

One can determine whether a contract involves a lease based on the aforementioned factors.

Accounting for Leases

According to IFRS 16, lessees no longer classify

- Lease Liabilities

- Right of Use of Assets (ROUs)

Initial Recognition:

Journal Entry Example

| Particulars |

Debit |

Credit |

| ROU Asset A/C Dr. | 61445.67 | |

| To Lease Liability A/C Cr. | 61445.67 | |

| (being ROU asset and lease liability recognized) |

Subsequent Measurement:

- Lease Liability: Every year, interest on the lease liability must be recognized.

- Right of Use of Asset: The lessee must account for this asset in the following period under IAS 16 and depreciate it every year.

| Particulars |

Debit |

Credit |

| Interest A/C Dr. | 6144.56 | |

| To Lease Liability A/C Cr. | 6144.56 | |

| (being ROU asset and lease liability recognized) | ||

| Depreciation A/C Dr. | 6144.56 | |

| To Accumulated Depreciation A/C Cr. | 6144.56 | |

| (being depreciation on ROU asset recognized) | ||

| Lease Liability A/C Dr. | 10,000 | |

| To Bank A/C Cr. | 10,000 | |

| (being lease liability repayments made) |

Transition Approaches to implement IFRS 16

Entities might take one of two approaches to implement the IFRS 16. They are as follows:

1. Full Retrospective Approach

This approach requires restatement of comparative periods and as a result, the presentation of a third financial statement in conformity with IAS 1

2. Modified Retrospective Approach

This method eliminates the need to restate comparison periods. At the start of the current accounting period, the cumulative impact of IFRS 16 is accounted for as an adjustment to equity.

Exemptions to IFRS 16

Yes, they do exist. For short-term leases of less than 12 months and leases of low-value assets, IFRS 16 does not require lessees to report assets and liabilities.

How is it presented in the Financial Statements?

- Statement of Financial Position: Right-of-Use assets are reported separately under Property, Plant, and Equipment (PPE). It must be measured every reporting period in accordance with IAS 16 or IAS 40, depending on the asset's nature. Lease liabilities are shown separately or with other liabilities, with a note indicating which line item they belong to. Every reporting period, the amount paid as a lease payment must be removed from the lease liability.

- Income Statement: Interest on lease payments will be accounted for alongside other finance charges, and the Right-of-Use Asset will be amortized.

- Statement of Cash Flows: Payments for leasing liabilities, as well as interest on those liabilities, will be included in financing activities.

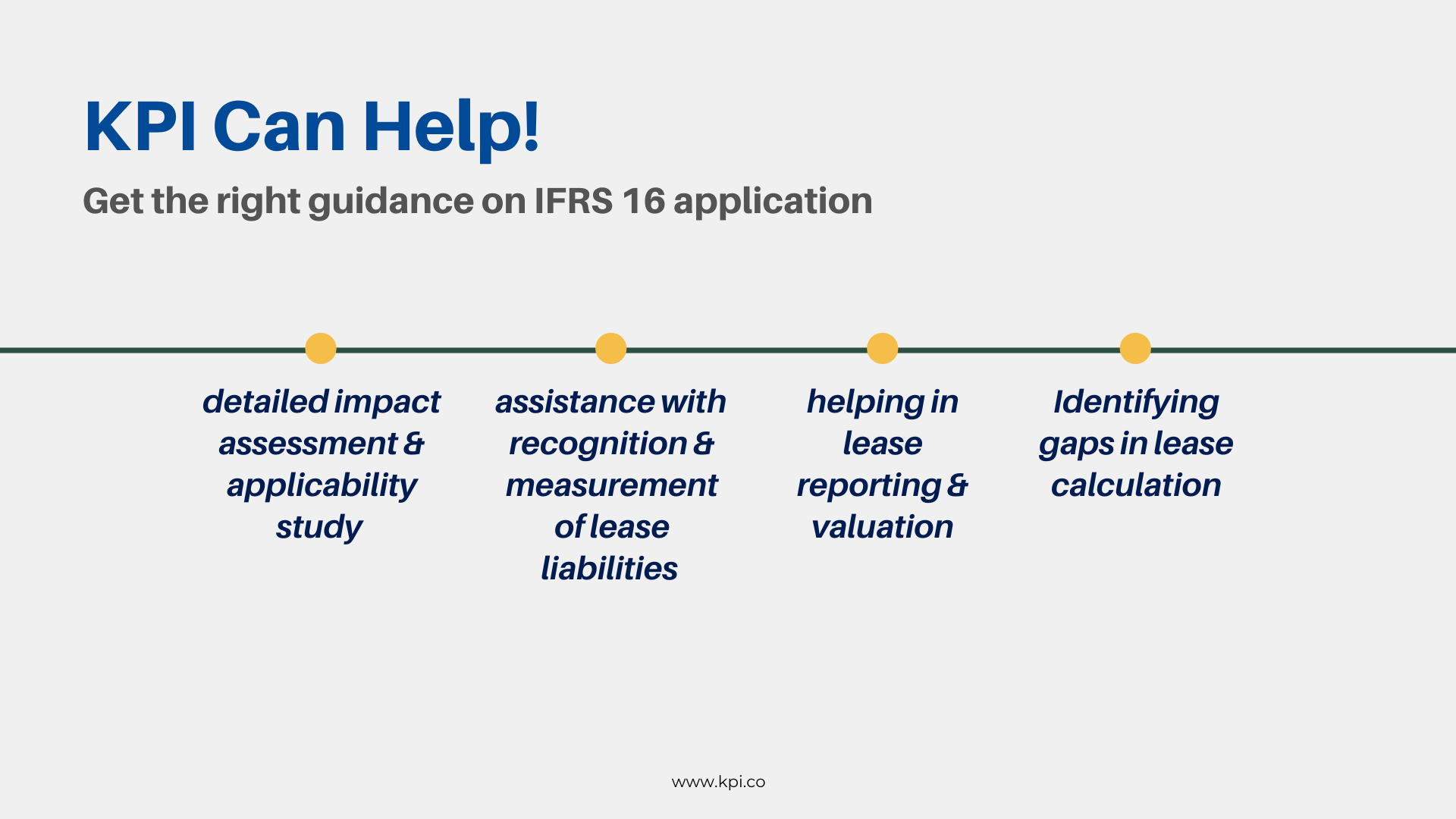

IFRS 16 Application - KPI can assist your business

Our accounting and auditing services can assist you to organize your lease administration and accounting processes. To maintain compliance and keep your lease accounting up to date, it's critical to understand and implement the IFRS 16 as soon as possible.